The key points from this article are:

- The Fed will control treasury yields

- Inflation is on the rise

- Real interest rates will fall in the second half of 2021

- As a result gold and silver prices will hit new all time highs in late 2021/early 2022.

Lately, I have been asked; why isn’t the gold price going up? We have near-zero interest rates, we have massive fiscal and monetary stimulus, we have historic budget deficits and federal debt, we have growing tensions between the world’s two largest superpowers, and we have a global pandemic that has impacted every nation and put economies around the world into recession. Surely the price of gold should be going through the roof?

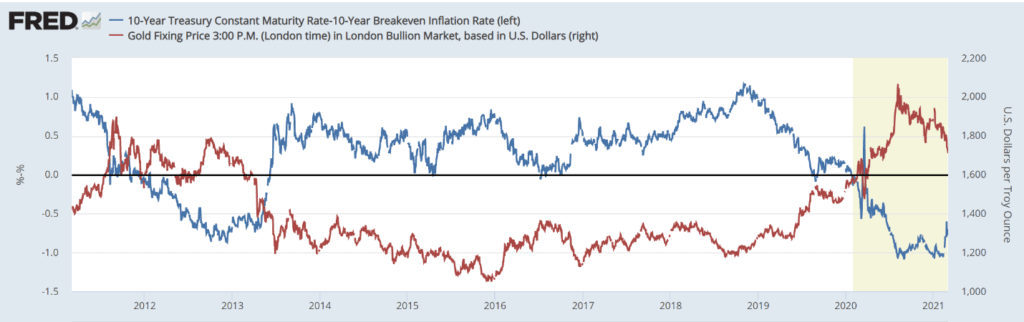

While sentiment, volatility and the risk environment are all capable of moving the gold price, there is one variable that has more influence over the price of gold than any other; real interest rates. Real interest rates are calculated by subtracting the inflation rate as calculated by the Consumer Price Index (CPI) from the long-term treasury rates (normally the 10-year treasury yield). The following graph shows the very strong negative correlation between the US$ price of gold and real interest rates.

Between August 2018 and August 2020, the price of gold rose by 73% in US dollars, going from $1,184 to $2,048. From those dates, real interest rates trended from plus 0.75% to negative 1.08%. However, since August 2020, real interest rates have moved sideways and since January of 2021, real rates have increased from negative 1.08% to negative 0.78% as of March 2. The impact of this rise in real interest rates since January 2021, has seen gold fall from US$1,943 to US$1,725 as of 2 March.

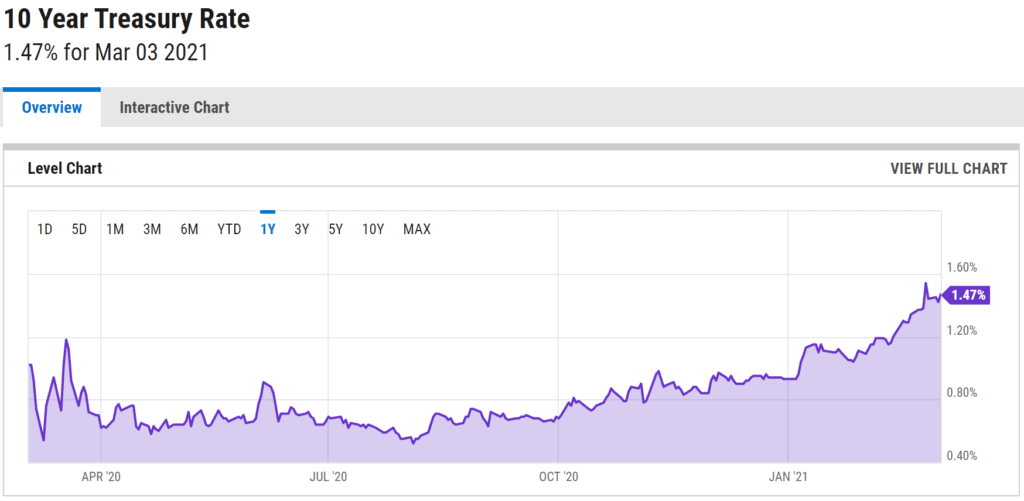

The driver for the increase in real rates has been the increase in the 10-year treasury yield, which increased from 0.93% on January 4, to 1.59% as of March 7.

The annual inflation rate in the US was steady at 1.4% in January 2021. The increase in the 10-year treasury was driven by market expectations of inflation increasing in the coming months. We are already seeing significant price increases in key commodities such as lumber, beef, and copper. A key area to watch will be the energy sector. US oil supply is currently constrained and a lot will depend on how OPEC manages to supply.

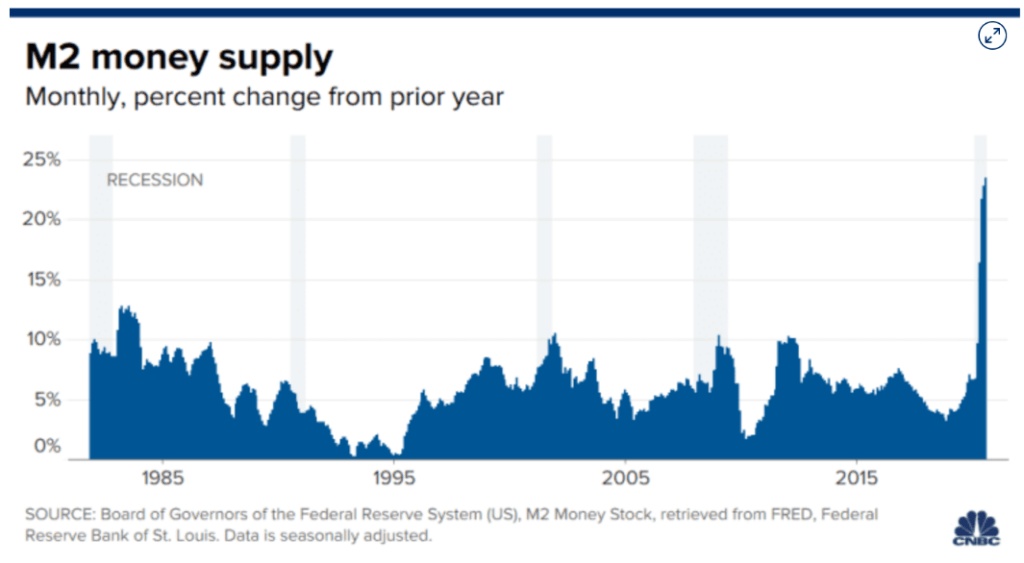

Transport supply chains around the world have been disrupted and shipping (container) rates are significantly higher. This has created supply backlogs in some markets. Fiscal stimulus packages will also be a major determinant of the level of inflation. On March 7, the US Senate passed a $1.9T stimulus bill including a $1,400 payment to every US citizen who earns less than $70,000, including children. Further stimulus packages are being discussed including a possible infrastructure package. Another factor contributing to inflation expectations is the increase in the US broad money supply over the last year.

M2 is up 25% in one year and this trend is likely to continue. The question is where will this money go? When velocity is low it tends to flow into financial assets such as equities. However, as the economy begins to recover from the pandemic, and we may see some scarcity of goods, then there is an opportunity for consumer price inflation.

On March 4, Federal Reserve Chairman, Jerome Powell, said the rapid growth in long term treasury yields was “notable” but he did not hint at any change in policy. However, to some extent, the Fed is in a box. US National debt has just hit US$28 trillion, there was a US$3.1 trillion-dollar deficit in 2020 and the forecasted 2021 deficit is US$2.3 trillion. Corporate debt in the US is US$10.5 trillion and non-financial private debt sits at US$27 trillion. The share markets historically high valuations are predicated on the current historically low-interest rates. If interest rates were to return to even the long-term mean, it would cause an economic disaster. Already we are seeing a rotation out of the growing tech stocks into value stocks as the 10-year treasury approached 1.5%. If interest rates were to continue growing unchecked, it could be a catalyst for a broader correction.

This high debt situation and the prospect of growing inflation is not dissimilar to the environment the US faced at the end of World War 2. Back then the US was running massive deficits to fund the war effort and debt was running at over 100% of GDP. They couldn’t afford to let yields rise even though there was inflation. So, they printed money and purchased treasuries in order to maintain the yield at 2.5%. At the time inflation was running in the double digits. They were able to bring their debt under control by essentially inflating it away.

I believe the Fed will be forced to look at some form of yield curve control if the 10-year treasury approaches 2%, particularly if the market reacts badly to the higher interest rates. The Fed believes that any uptick in inflation will be short term and will eventually drop back down to more recent norms. They are comfortable to see inflation go beyond the 2% given their confidence that they believe it can be controlled and brought back into line.

Since August 2020, interest rates have been on the rise, while inflation was muted, resulting in real interest rates trending up. This has been a negative influence on the price of gold. However, with inflation now predicted to rise, and with the prospect of long-term interest rates being suppressed, we may see real interest rates trend back down in the second half of 2021. If this does play out, we are likely to see gold and silver hit new historic highs.

Disclaimer: This article is an opinion piece and as such, it should not be taken as investment, tax or legal advice and nothing provided in any materials by New Zealand Vault should not be construed as such. Before undertaking any action, be sure to discuss your options with a qualified advisor. The information in this article is based on the best research available to date, however, due to the ever-changing landscape of the world economy and the growing developments in world politics, this information may become out of date relatively quickly. Please verify all facts and get in contact with us if you have any issues with our content.